Table of Contents

- 1. Introduction

- 2. Innovation vs. Economic Growth

- 3. Historical Context: Innovation as a Catalyst for Growth

- 4. Key Findings

- 5. Supporting Data

- 6. R&D Investments: Their Relevance

- 7. Innovation Ecosystems: Fostering Growth

- 8. Case Study: Silicon Valley

- 9. Government Initiatives

- 10. Job Growth and Economic Restructuring

- 11. Automation as a Challenge

- 12. Conclusion

How Much Does Innovation Drive Economic Growth?

Introduction

Innovation has always been one of the most important engines of economic growth. From transformative technologies to incremental improvements, innovation shapes economies by improving productivity, creating jobs, and boosting global competitiveness. This paper will present how much innovation contributes to economic growth on the basis of data-supported insight and more specific examples.

Keyword: innovation drive economic growth

Innovation vs. Economic Growth

Before we demonstrate how innovation influences the growth of economic development, we have to explain what each term means.

- Innovation: A set of processes that allows for improved product, service, or even process development-from minor incremental changes to radical new technological advances.

- Economic growth: The process whereby there is an increase in the production of goods and services within a national setting; generally expressed in terms of an increase in real gross domestic product.

Historical Context: Innovation is a Catalyst for Growth

History has countless examples of how innovation has sparked an economic avalanche:

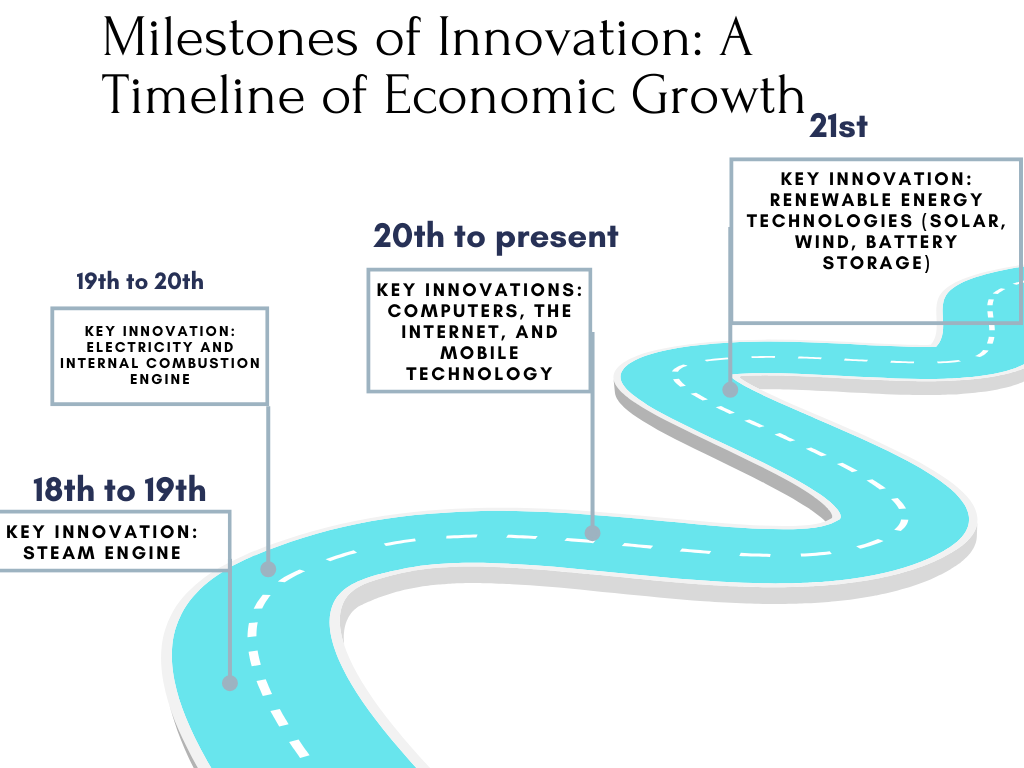

- The Industrial Revolution: Due to innovations like the steam engine, production increased to an all-time high, resulting in the most striking GDP growth.

- The Digital Age: The advent of computers and the internet into business and industry produced an unprecedented level of productivity gains and economic output.

Industrial Revolution

Time Period: Late 18th-19th Century

Key Innovation: Steam Engine

Impact: Revolutionized manufacturing and transport; mechanization, mass production, and factory-based work.

Economic Growth: Increased GDP and urbanization, especially in Europe and North America.

Second Industrial Revolution

Time Period: Late 19th to Early 20th Century

Key Innovations: Electricity and Internal Combustion Engine

Impact: Increased productivity in industries and led to the emergence of new industries, such as automotive and steel, while boosting the production of various consumer goods.

Economic Growth: Accelerated global economic growth and set in motion the present capitalism.

Digital Era

Time Period: Late 20th Century to Present

Key Innovations: Computers, Internet, and Mobile Technology

Impact: Enabled automation, improved communication, and paved the way for industries like IT, e-commerce, and fintech.

Economic Growth: Caused globalization, improvements in productivity, and significant GDP growth in tech-led economies such as the United States, South Korea, and China.

Green and Renewable Energy Revolution

Time Period: Twenty-First Century

Key Innovations: Renewable Energy Technologies (Solar, Wind, Batteries)

Impact: Shifted away from fossil fuel dependency towards sustainable energy sources and promoted sustainable industries.

Economic Growth: Created jobs in the green sector, encouraged nations to reduce carbon footprints, and stimulated investments in clean technology.

Key Findings

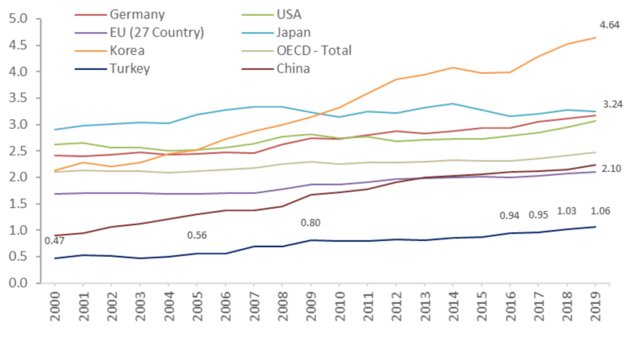

Various studies showcase a strong link between innovation and economic development. Consider the OECD study, which has unearthed that an increase of 1% in innovation investments leads to a 0.3% increase in GDP.

Supporting Data

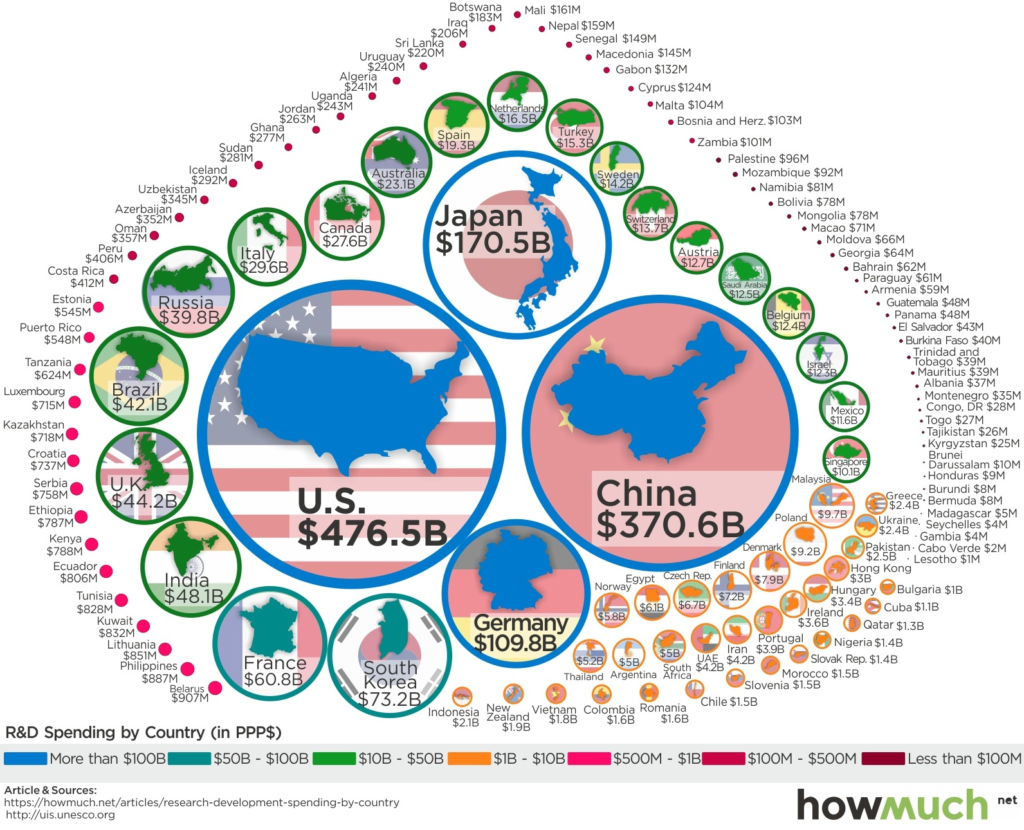

- Global Innovation Index: High-ranking innovative countries, such as Switzelrand and South Korea, often maintain a lead over their contemporaries in GDP increases.

- R&D Expenditure: Countries like the USA and Germany favor long-run economic benefits for heavy investment in research and development.

R&D Investments: Their Relevance

Innovation is at the heart of research and development (R&D); firms or governments which plow in heavy sums into R&D generally receive their money back in terms of new technologies and gradual economic growth.An example: Aggressive R&D spending has made South Korea quite the technology and economy powerhouse.

Innovation Ecosystems: Fostering Growth

An innovation ecosystem-a constellation of startups, established corporations, academic institutions, and policies of the state-is one of the key pillars supporting economic growth.

Case Study: Silicon Valley

This unique mix of capital, talent, and risk-taking, has maintained the Silicon Valley’s position to grow the economy continuously.

- Government Initiatives: Incentives like tax credits and grants may also stimulate innovation and thus fuel economic growth.

Job Growth and Economic Restructuring

Job Growth

Innovation increases not only the level of productivity but also gives credence to the development of new job markets. In the various fields, need for technical skills gives rise to millions of jobs.Innovation is expected to drive productivity growth by making available new technologies, new processes, and new services in order to add efficiency and create value. It also creates entirely new markets for jobs. The more industries change, the more such industries require specialist technical skills, leading to another million new places of work. The spotlight on how innovation reshapes productivity and job options is thus on technologies from tech and healthcare to renewable energy and artificial intelligence.

Automation as a Challenge

While automation drives innovation and increases efficiency, this also comes as a challenge since many jobs that were previously done by humans have now become outdated. As machines and algorithms take on all monotonous and repetitive tasks, job losses may come in some sectors. But this can be countered by the deconstruction and conversion: an ongoing transition where outdated jobs gradually phase out while at the same time providing for renewed job trends for the larger workforce to feasibly make possible the reskilling and upskilling of the job-seeking population.

A good balance must strive for investing in educational and training programs that equip individuals with technical skills supporting their movements into emerging job markets. Governments have to work closely with businesses in supporting displaced workers through these transitions and consider themselves responsible for ensuring that innovation translates to long-term growth. By instilling a culture of continuous learning and trainability, societies can let automation in while ensuring long-term employment and economic stability.

Success Stories:

India’s digital payment transformation, in particular, through the Unified Payments Interface (UPI), has played a determining role in advancing financial inclusion and driving economic activity. UPI has simplified and democratized access to financial services by enabling millions of individuals, especially in rural areas, to carry out seamless, real-time financial transactions with their mobile phones. This has enlarged access to banking, which means enabling people to participate in the economy without the need for actual physical bank branches.

It has contributed to greater financial inclusion through online payments for transactions, savings, investments, and even access to credit. UPI bridged the gap by providing people seamless and direct access to financial services.

Through this transformation, the inflow of money into the economy has triggered economic activity, fueled digital entrepreneurship, increased financial cost-efficiency, and enhanced transparency. UPI, therefore, has emerged as a beacon for India’s economic growth by promoting efficiency, innovation, and inclusive development.

Barriers:

The evaluation of funding sources and technologies, which are poorly spread-out within many communities or markets, represents major challenges to innovation. Inadequate funds may impede entrepreneurs and businesses in their efforts to develop, scale, or adopt innovative technologies, which very often leads to a limitation in their ability to pursue innovation. This invariably means that projects sometimes get stuck in an old-age stage-or underfunded and with very little capacity for research and development.

Lack of access to technologies is another confounding dimension of this problem. In middle-income countries with infrastructural deficits or digital divides, potential entrepreneurs or the broader population may lack the means to leverage advancements in automation, digital services, or e-commerce. Such limitations tend to perpetuateregional apathy from the global innovation trend, which typically creates a cycle of underdevelopment.

To counter these threats, investments in both financial resources and technological infrastructure are necessitated. Governments, private sector partners, and international organizations must urge funding, promote technological adoption, and create an ecosystem that favors the proliferation of innovation. In dealing with such challenges, the region could liberate its potential for sustainable growth and development.

No responses yet